The 4 Unique ATS Models of Trading Secondaries

The ATS (alternative trading system) promises secondary market trading for private assets. Here is how the various models actually work.

By Vertalo Team

We remember back in January of 2018 when we stumbled across an article about what blockchain technology could do for private assets and capital markets. From asset tokenization, to automated KYC via smart contract, to secondary trading, this article laid out the vision of private markets that many of us had shared for a long time.

Note: We’ve tried to find that article, we believe it was Forbes, but it could have been another large financial publication, but we cannot seem to locate it. Another otherwise great piece of content lost to the vast internet. 🤷♂️

Assets that could trade between users, middlemen being cut out due to optimization of technology, processes being streamlined, the list was impressive, and probably threatening to many who operate in this space. We’re just now seeing those promises fulfilled, and it’s the reality of how this industry works that we want to highlight here.

The boom of blockchain-enabled securities has really focused on a singular vision: Liquidity.

It’s the challenge for the entire private asset market. The private markets are anywhere from 3-5X larger than the public markets, but are 400-500X less liquid. The private capital markets raise double the amount of capital, and yet are hundreds of times less liquid.

(Source: Harmonization of Securities Offering; Setter Volume Report FY 2018, World Federation of Exchanges database Note: Figures as of 2019).

Private markets are plagued by:

Systemic friction

Information asymmetry

Siloed information (investors don’t know where to look to find interesting deals, if you’re not an insider, you simply don’t hear about it)

Paper processes that are outdated, unnecessary, and irrelevant (looking at you Medallion Signature Guarantee, or the drawn-out ROFR process)

Lack of liquidity

Illiquidity discounts (these instruments stay locked up, so the only buyers that want to buy do so at a large discount, leaving the seller with no option but to take a substantial discount to NAV to unwind their position)

Note: the typical method for secondary liquidity is through secondary market transfers and trading, whereas we believe the future method will be collateralized lending against privately held assets. That brings its own challenges, for this piece we’ll focus exclusively on secondary trading as the fulfillment of the liquidity promise.

Currently, if you want to transfer or trade a privately held asset maintained entirely by the issuer, you’ll be stuck with a papered process that can take weeks, or even months, to complete. Can you imagine getting a notification from Fidelity, Robinhood, or Schwab multiple weeks after the fact that the sell order you posted had been settled?

The Illiquidity Discount

The penalty for private assets that are illiquid. We’ve spoken with real estate operators whose investors suffer from the illiquidity discount if they ever come to unwind their position. In one case, an investor who had bought into an otherwise stable and solid commercial real estate asset ended up with a 38% discount to NAV in order to liquidate his position early. Insane.

Also, companies are staying private for longer

The most straightforward and understood method for liquidity is to go public. But this brings specific challenges too. We know for a fact that Intel’s legal and investor relations teams spent between $3-5 Million dollars per year on filing requirements and public company reporting compliance alone. And that’s perfectly in line with what the research reflects.

Simply put - it’s expensive to be a public company. There are filing requirements, disclosures, investor protection provisions, added personnel to support this compliance, you name it. Due to this, increasingly, we are seeing companies stay private for longer. Commissioner Caroline Crenshaw of the SEC noted that “The number of private companies is growing and they are staying private for longer….” in April 2022 in her remarks at the symposium on private firms.

History side note: With public companies, the Securities Exchange Act of 1934 outlined the requirements and required registration of stock exchanges on a national level. Before this, many cities in America had their own stock exchanges. Even obscure places like Salt Lake City had their own stock exchange known as the Intermountain Stock Exchange. San Francisco similarly had their own Stock & Bond Exchange. Kinda neat.

If we can solve the liquidity problem, it stands to reason that we could eradicate, or at the very least, dramatically reduce, the illiquidity discount that often plagues private markets.

The question here is, how does one attain liquidity for private held assets? They are, after all, securities, and thus must be treated as such. This means that simple blockchain enablement via the ERC20 or similar standard will not work. The upgraded and enhanced treatment of these instruments is required, since they are not widgets you are buying on Shopify, but securities, subject to all securities regulations that have been established. This includes investor protections, anti-money laundering checks, know-your-customer rules, and many others.

We can’t tell you how many conversations we’ve had with operators who are passionate and believe blockchain can solve the liquidity problem for a private asset, like real estate, only to learn that since these are securities, the treatment is completely different from cryptoassets like Bitcoin or Ethereum. Many ask about enabling decentralized trading of these assets, like on a Uniswap or SushiSwap type of exchange, but that isn’t legal in the United States. Indeed, Kim Kardashian’s $1 Million Fine Could Impact Uniswap, SushiSwap And Other Decentralized Exchanges.

A famous example of securities trading outside of a regulated exchange was in 1999 when the SEC filed suit against 3 Individuals for attempting to sell securities on eBay.

eBay is not a registered stock exchange or brokerage firm. By law, you cannot sell securities on their platform just like you can’t sell them on Binance, Coinbase, Uniswap or any other crypto exchange. The matching of buyers and sellers for securities transactions is a highly regulated activity. So the question stands - how can we attain liquidity for private assets without acquisition or IPO?

Enter the alternative trading system (ATS).

We won’t get too detailed into the history of alternative trading systems, although a good friend wrote an outstanding piece on Alternative Trading Systems, feel free to dig into his treatment of them there.

At a high level, ATS operators are registered members of FINRA, they are broker-dealers, and are subject to reporting compliance and standards similar to national stock exchanges, although admittedly the reporting standards are less stringent than stock exchanges like the Nasdaq or NYSE.

At their core, ATS’s have the regulatory ability to match trades of buy and sell orders between investors in an asset. This trading activity is one of the primary ways the digital asset ecosystem is seeking to solve the liquidity challenge. Like a “mini IPO” of sorts, where the issuer can list on an ATS but still remain a private company.

Since the introduction of blockchain-based securities trading on ATS’s, FINRA has released two different models for how to trade and settle tokenized private assets compliantly. These are the 3 Step Process and the 4 Step Process.

We believe the real intent in laying out the 3 vs. the 4 Step processes comes from a desire to separate interests and responsibilities for the various actions that occur within the trading and settlement processes. Indeed Gary Gensler himself has commented on the problematic fact that crypto exchanges are unilaterally performing the following functions:

Order matching & trading

Clearing & Settlement

Collateralized lending

Account management (largely a brokerage function)

Cash management & money transfer agency

In the world of securities, these functions are almost all distinct and performed by different entities, which helps to separate and divide the interests of each party involved. Most investors are unaware of this fact, since technology, integration, and a lot of existing infrastructure makes the purchase, sale, lending, margin, trading, clearing, and settlement, of securities seamless and easy. ATS’s operate within the existing FINRA frameworks to divide the interests of these activities and legally trade, settle, and clear securities.

Here is how both processes work.

FINRA 4 Step Process

Step 1. The buyer and seller send their respective orders to the ATS

Step 2. The ATS matches the orders

Step 3. The ATS notifies the buyer and sellers of the matched trade

Step 4. The buyer and seller settle the transaction bilaterally, either directly with each other or by instructing their respective custodians to settle the transaction on their behalf.

In the 4 Step Process, buyer and seller are required to interpose themselves, not only to initiate a trade as you’d expect, but also to confirm that cash should move. They either interact with one another directly for the purposes of moving the cash from buyer to seller, or instruct their custodian(s) to enact the movement of money, after which the securities can move from seller to buyer.

This creates enormous friction and an unpleasant user experience, since it introduces counter-party risk. ATS’s that operate this model typically create rules around the communication of cash settlement, in order to facilitate trades more seamlessly. If buyers and sellers in this process are institutions, brokers, banks, or other large players, this isn’t as much of a problem since there will be an employee (or team) who’s job it is to handle these instructions. It’s the retail case where this model displays its ineptitude. Imagine instructing retail investors to a. send cash to the seller, and b. send the security to the buyer, OR to post a trade, then confirm with their custodian or on their own that it was legitimate and yes, please allow the movement of cash & securities. Not an ideal user experience.

FINRA 3 Step Process

Step 1. The buyer and seller send their respective orders to the ATS

Step 2. The ATS matches the orders

Step 3. The ATS notifies the buyer and seller and their respective custodians of the matched trade and the custodians carry out the conditional instructions

The difference here is that the ATS, not the investor themselves, is able to instruct the custodian to move cash and securities respectively. It’s simpler and produces a far better user experience that is closer to what retail investors have come to expect from public markets. It also reduces the counter-party risk introduced in the 4 Step Process, since instructions are sent to to the custodial partner, who can follow them explicitly thereby reducing the possibility that buyer or seller back out of the trade after it’s been initialized. We expect the lion’s share of the growth in the digital asset securities industry to be through ATS’s using the 3 Step Process and automating the process on behalf of retail investors.

Remember the cardinal rule of user experience - “Don’t make me think.”

Before we dig into the models themselves, there are several critical elements that must be considered when examining how securities are traded and settled, in both the 3 and 4 Step Processes. Those considerations are:

Good Control Location

Cash Settlement

Update Balance Instructions

Asset Custody

Good Control Location

We’ve written on the Good Control Location (GCL) in a previous post, but this strikes at the heart of the SEC’s goals to protect investors. It includes provisions that protect investors from their securities being lost, destroyed, or otherwise changed without authority. It also includes provision for the ability to unwind an illicit trade, or enact a transfer outside the permission of the investor (like an orderly estate transfer after death, for example). This is what makes digital asset securities so radically different from ERC20 digital bearer instruments on-chain.

The question here is, who maintains the Good Control Location over the securities? It can be:

a custodial broker

the transfer agent

the issuer themselves

or a registered custodian, wholly separate from the broker

Additionally, if the broker applies a custody model, there may be a “split ledger” situation whereby some of the ledger, and its associated Good Control Location is held by the Transfer Agent, and the GCL over deposited shares at the ATS are maintained by the custodial broker.

This custodial deposit function highlights the difference between beneficial and street name ownership, and it brings its own challenges of shareholder management and communication, but also additional benefits. The challenge is that there is no centralized ledger of full beneficial ownership but rather a fragmented one, because of how the deposit process and street name ownership works. If an issuer wanted to list your asset on multiple ATS’s for added liquidity and market exposure, the maintaining of your list of beneficial shareholders would become very tedious very quickly.

This is one of the biggest problems that public markets deal with, which we will give adequate treatment to in another post.

Cash Settlement

The second critical element is who handles cash settlement? If the broker is self-clearing, they can handle cash themselves. This eliminates the need for an outside custodial party and can simplify integration efforts between distinct entities, like the Transfer Agent, clearing broker, and ATS. For blockchain-based securities, the SEC does not allow a Broker-Dealer to perform cash settlements, thereby introducing unnecessary inefficiencies into this process.

If the broker is not self-clearing, this responsibility would fall to a custodian that is registered as a Licensed Money Transmitter or Money Service Business (MSB). They would be responsible for the movement of cash from buyer to seller, and relaying that information (purchase amount, date, confirmation of the movement itself) to the broker. This information must be recorded for securities purposes, as well as reporting & compliance. FINRA requires ATS’s to record and report on failed trades, for example.

Update Balance Instructions

The next critical element for consideration and is the core difference between the 3 Step and 4 Step Processes. Where do the instructions come from, which party, and what sort of sign-off or regulatory licenses are needed to certify legitimacy?

The reason this makes the cut as a critical element is that “update balances” is the same as certifying ownership changes - changing the cap table and recording new shareholder ownership. Once a share is owned by an investor, they have special protections and rights, as outlined by the capital stack and defined through the nature of the instrument and/or PPM or offering memorandum (is it profit-sharing, does it carry voting rights, etc.) Beyond these standard measures, shareholders usually have more firm and distinct grounds for legal recourse should they deem that necessary.

Asset Custody

Is the broker-dealer a custodial broker under the customer protection rule, 15c3-3?

Finally, we come to matter of custody. If the brokers take custody of the asset, and it’s a security token on-chain, they have to have blockchain infrastructure to support the proper custody and ledger management of the asset itself. This has been a huge hindrance to the growth and adoption of the digital asset securities industry, since many large brokerages, like all large companies, struggle to adopt new technology and build with/around it. It is growing though, as companies like Fidelity, NYDIG, Nasdaq, BlackRock, and others, are building digital asset strategies and engaging with the opportunity in this space.

Now that we’ve clearly identified the factors for consideration, let’s look at the each of the four models and consider how they work with regards to the required parties involved and the investor experience.

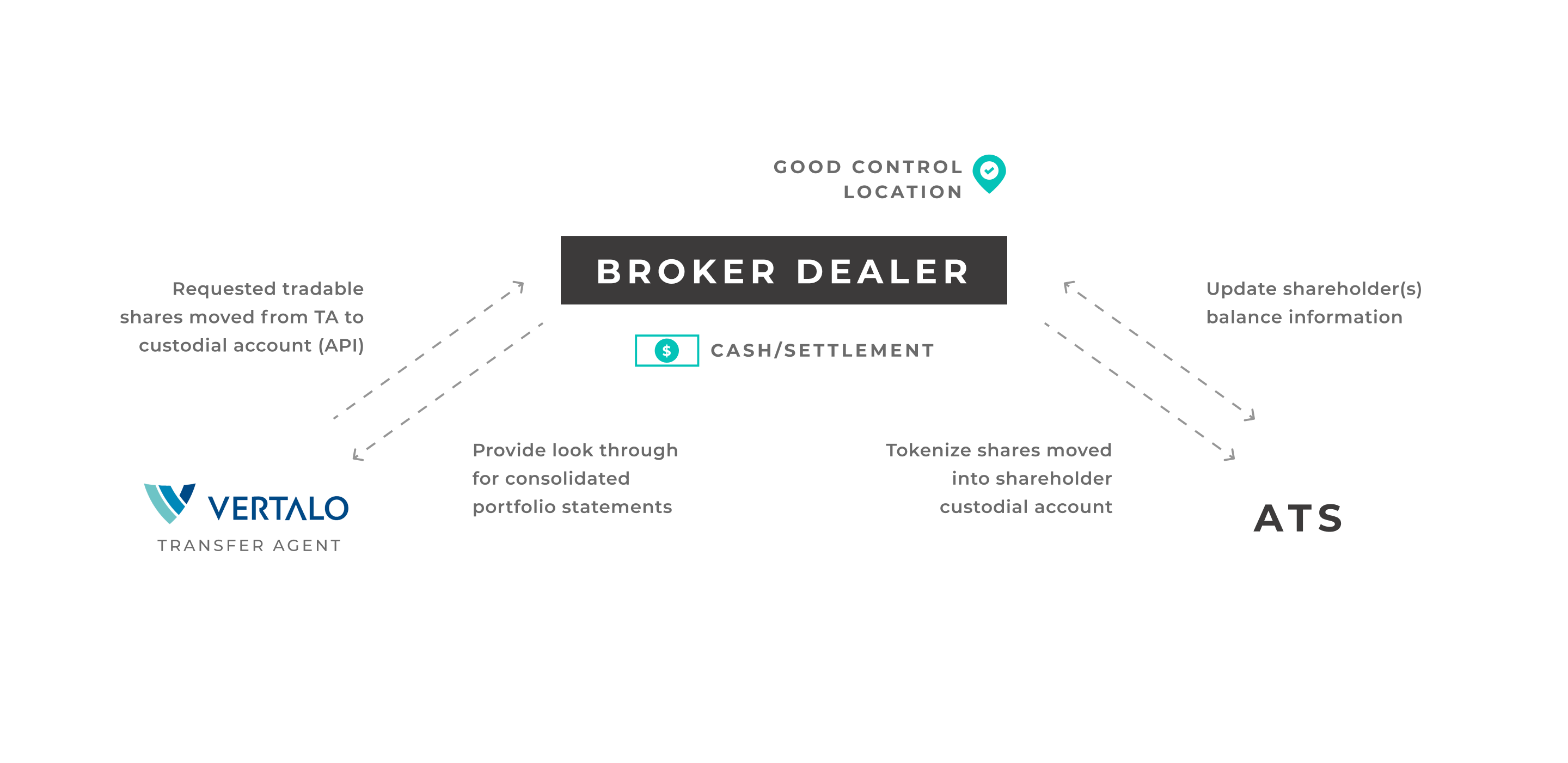

Model 1: Self Clearing Custodial Broker

In this model, we see a unique corporate structuring that allows the same parent company the ability to custody the securities under the Broker-Dealer entity, and then handle trading and order matching through the registered ATS. The parties are separate and distinct, but the Transfer Agent > Broker-Dealer integration, and subsequent end user experience, are much more seamless and pleasant.

In this model, the ATS simply exists to match orders between buyers and sellers, the rest of the process is handled in the Broker-Dealer’s environment.

Investors start either at Vertalo with a request for deposit, or at the broker-dealer themselves. With express permission from the issuer, Vertalo collects the deposit request from the BD on behalf of the investor. There are a number of elements we gather to ensure it is the investor acting themselves (collect signatures, confirm information like address and email address match, the ATS partner uses 2FA upon login, etc.) that allow us to streamline this process.

Investors request deposit (either at Transfer Agent or from the BD directly)

Transfer Agent receives the deposit request

Transfer Agent verifies all information is accurate

Deposit is submitted, cap table is incremented to reflect Street Name Ownership of the custodial broker

Investors submit orders on Broker Dealer

Orders are relayed to ATS

Order match occurs at the ATS

Settlement instructions are sent back to the broker-dealer

Broker settles transaction through moving cash and securities respectively

Trade is complete

Once deposited, the Broker Dealer holds the securities in Street Name ownership, and can handle the movement of cash and securities once orders are matched on the ATS. Since this is the same parent company, these integrations are easy to maintain, and the investor doesn’t have to log in to multiple locations to initiate the trade or send instructions.

Model 2: Non-Custodial ATS, Custodian Takes Deposit of Securities

In this model, the custodian is the king of the settlement process by handling the custody of securities and movement of cash between buyer & seller in the secondary transaction. The ATS fulfills order matching, and the ledger is kept, but only contains the names of those who are registered shareholders, since the line item entry for all shares held through the custodian are listed in the name of the custodian.

Like Model 1, there is a depository process whereby the investors balances are moved from the Transfer Agent to the Custodian. This allows the ATS to query those balances before a trade is initiated to guarantee that shareholder is, in fact, long the balance they wish to sell. For any investor wishing to purchase, no such query need take place, although there may be restrictions that would necessitate that, such as a pull to see if a shareholder is restricted or otherwise barred from purchase. A common example of this is when employees are not allowed to own more than X% of voting shares of a company.

Here’s what the flow typically looks like in this model:

Investors deposit shares to the custodial account

Investors link their custodial account to the account at the ATS

this linking can be done asynchronously to the account creation at the ATS

Investors log in to ATS and submit buy/sell orders

ATS queries custodian to confirm the selling investor is long the shares they want to sell, receives confirmation or rejection of the request

Order is matched on the ATS

ATS instructs custodian to move shares & cash respectively, receives notification that is has been done per the instructions

Trade is complete

The “Update Balance Instructions” you see from the Custodian to the Transfer Agent is reflective of when investors wish to remove their shares from custody and transfer them back into their name directly. In this case, the investor’s share count is deducted from the omnibus custodial account, and they are added as the Street Name Owner of the security. This is not required, most investors would likely leave their shares in the Street Name Ownership of the custodian, but could still happen if the investor was keen to hold the securities in their name, say for shareholder voting purposes where the investor didn’t want the custodian to cast their vote as a proxy for the investor.

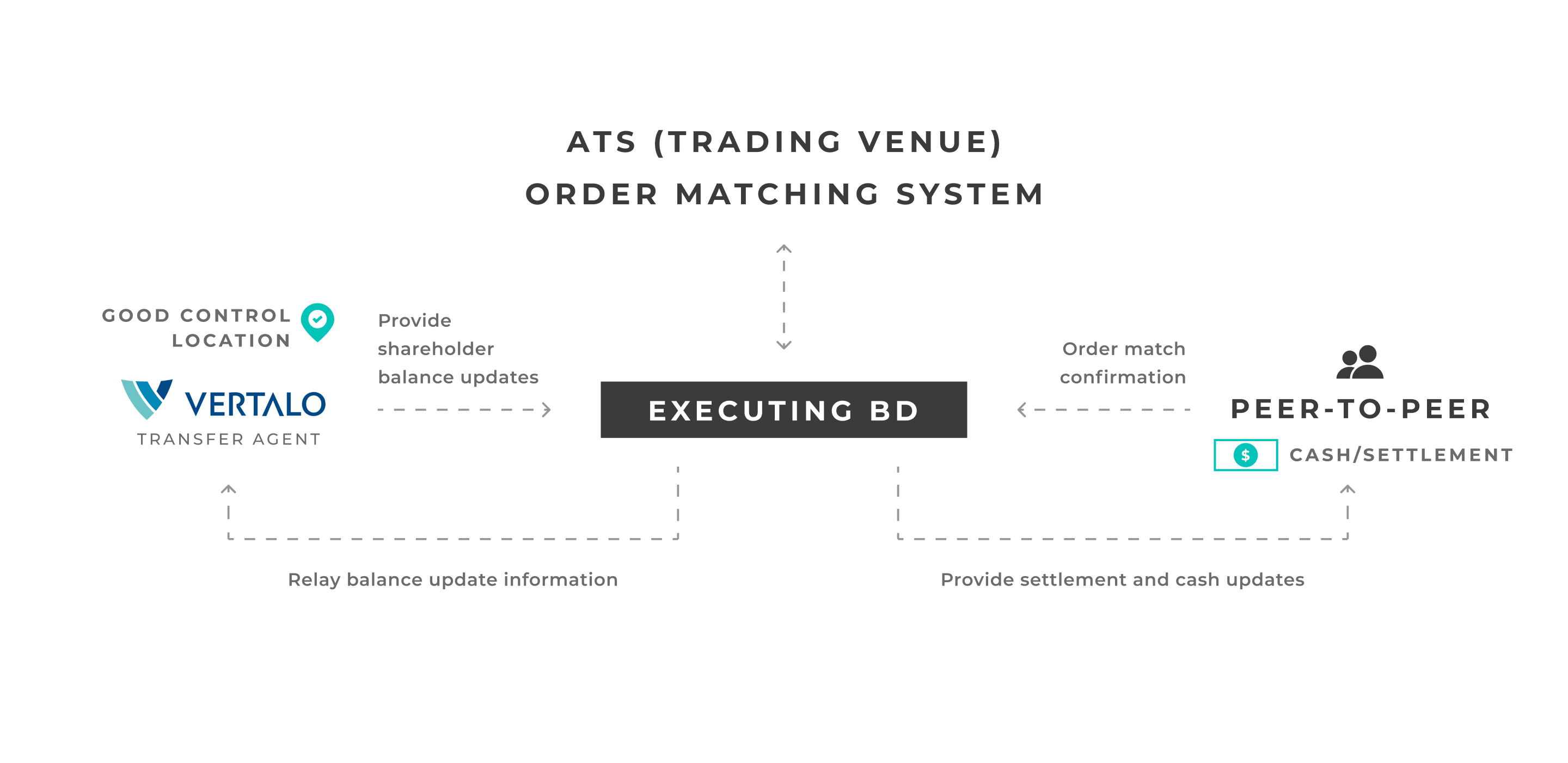

Model 3: Non-Custodial BD, Same Corporate Entity Behind BD & ATS

This model uses the 4 Step Process, requiring investors to settle cash between one another. Otherwise, it’s similar in nature to Model 1, in that a parent company holds both the broker dealer and the ATS, even though they are distinct and separate legal entities.

In this model, the steps are functionally the same as the previous models with regards to order matching, except that rather than query a custodian for long balance information held by investors, the broker queries the Transfer Agent directly, since they are responsible for the maintenance of Good Control Location.

The flow of steps might look like this:

Buyer submits a buy order, shareholder submits a sell order

*buy & sell orders can be asynchronous and unrelated to one another

The executing broker queries the TA to confirm the seller is long the number of shares they want to sell

Orders are sent to the ATS for match

Orders are matched

Confirmation thereof is sent to the executing broker

Broker informs buyer and seller for the purpose of cash settlement

Buyer & seller handle cash settlement between one another directly

Cash settlement is confirmed to the executing broker

Broker instructs Transfer Agent to update the cap table with the requisite trade information (buyer information, purchase info, etc.)

Trade is complete

The critical difference here is that since there is no custodian involved, there is no deposit process, and the Broker can communicate directly with the Transfer Agent for the purposes of maintaining the cap table and shareholder ledger.

The obvious flaw here is that of user experience, since the investors have to deal directly with one another for the movement and settlement of cash. The benefit, however, is that the Transfer Agent is always aware of what the shareholder ledger looks like. This is especially important should an issuer want to list on multiple ATS venues. We’ll write more on this specifically in a future post.

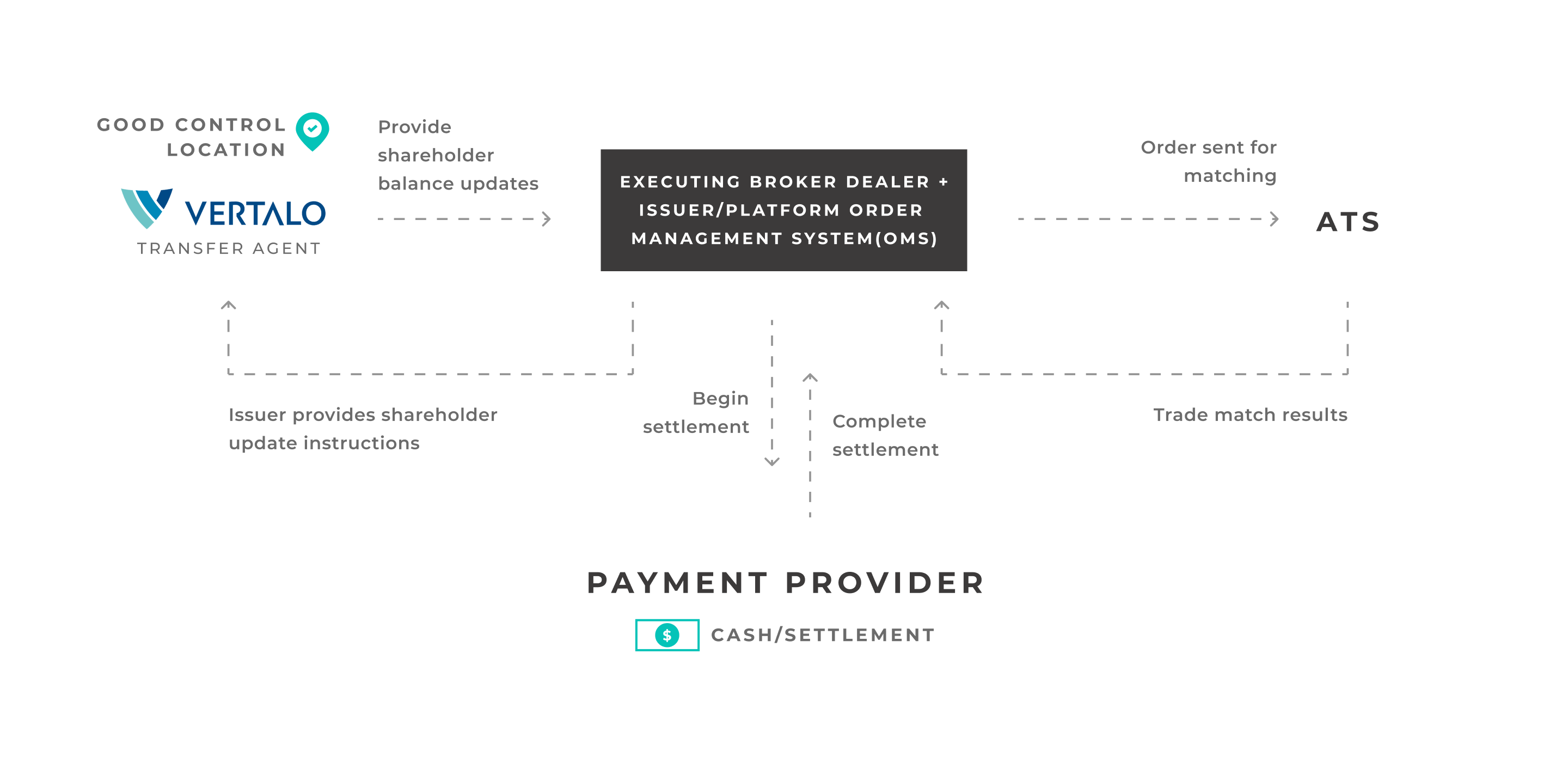

Model 4: Order Match via Order Management System (OMS)

Model 4 looks like Model 3 except for two critical differences:

The executing broker has no formal relationship to the ATS, they can be completely separate and distinct companies with no shared parent company.

The broker was also the same one involved in the primary issuance of the security, meaning that suitability checks and KYC information has already been collected from each investor.

This model is also unique, because rather than a custodian handling the Good Control of the securities, that responsibility is held by the issuer themselves. Many issuers seek to hire out this role, since it’s so critical, and doing so improperly often bears hefty fines and problems with audit and filing with the SEC.

Here’s what the flow could look like in this model, this assumes the investor account has already been setup and suitability has been handled by the broker:

Buyers and sellers send their respective orders on the issuer platform

Issuer relays the orders to the ATS, including the broker ID

Orders are matched on the ATS

Order match confirmation is sent to the Broker & Issuer

Issuer sends cash settlement instructions to the payment processor

Once cash movement is confirmed, the issuer sends “Update Balance” instructions to the Transfer Agent

Transfer Agent confirms the share transfer is properly documented, then documents the move of shares from seller to buyer

Confirmation of the transfer is sent to the issuer

Trade is complete

We have seen this model often used for issuers seeking to create liquidity and platforms that buy, sell, and trade private assets in context on their own websites. Rally Road is a prime example of where this model functions very well from a regulatory and user experience standpoint. Rally uses North Capital’s PPEX ATS, and has partnered with Dalmore for the Broker Dealer requirements, who was also the broker of record for their Reg A+ filing process. We’re unaware of who Rally uses for payment processing, but this model also necessitates a payment processor (typically a tech-enabled provider like Dwolla) to handle the movement of cash for securities via API integration.

Conclusion

The realities and subtle nuances of each of these models are still being discovered as the operators in the ecosystem grow together, integrate with one another, and bring on new issuers both large and small.

It’s been a real pleasure to have a front seat to exactly how these models behave and the impact it has on issuers and investors. We hope this was valuable for all you readers too. Feel free to subscribe (it’s free!) for more content like this around the digital asset ecosystem, private capital markets, finance, and blockchain.

Till next time.

Disclaimer: None of this information is nor should it be considered as professional, legal, investment, or any other sort of advice or recommendation. The information presented herein is done so for informational, entertainment, & educational purposes only. Please consult an attorney or licensed investment professional before taking any investment or professional action.